By crossing the €100Bn euro mark for the first time, European venture capital has set a record in 2021. One year later however, the economic context is much gloomier. As of June 17, the Nasdaq 100 Index has fallen by 32.2% and the STOXX Europe 600 by 10.8% YoY.

With a lag time, private markets are also preparing for a difficult period. With a foot on both sides of the Rhine, XAnge is well positioned to analyze trends in the VC market in France and Germany.

Germany crashes first – late stage drives the trend

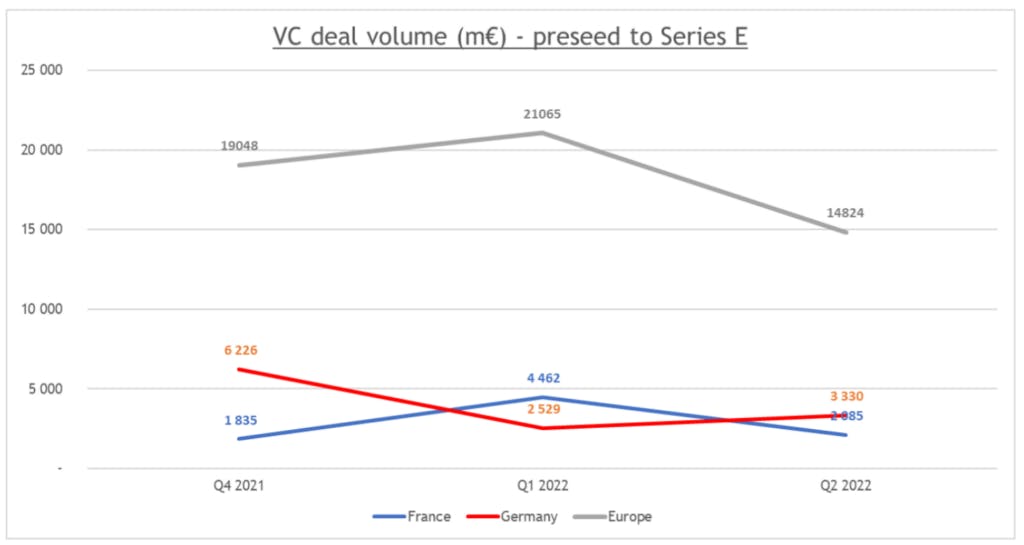

2022 was off to a great start for European startups and VC funds as January scored very high. France even hit a record with €2.7Bn invested and six new unicorns: Qonto, Back Market, Exotec, Payfit, Ankorstore, and Spendesk. February and March followed well above 2021. US funds such as TCV, Tiger or General Atlantic participated in all 4 mega rounds (> €100m): Alma, Doctolib, Deepki, and Akeneo. Over Q1 as a whole, Europe remains quite stable with +10% in terms of volume and -10% on the number of rounds. But the wind quickly changes and the first alarm bells are ringing by shrinking exits. As tech companies’ shares drop, IPOs become rare and only account for €9.1Bn over Q1 – compared to €63Bn the previous quarter.

Source : Crunchbase[/caption]

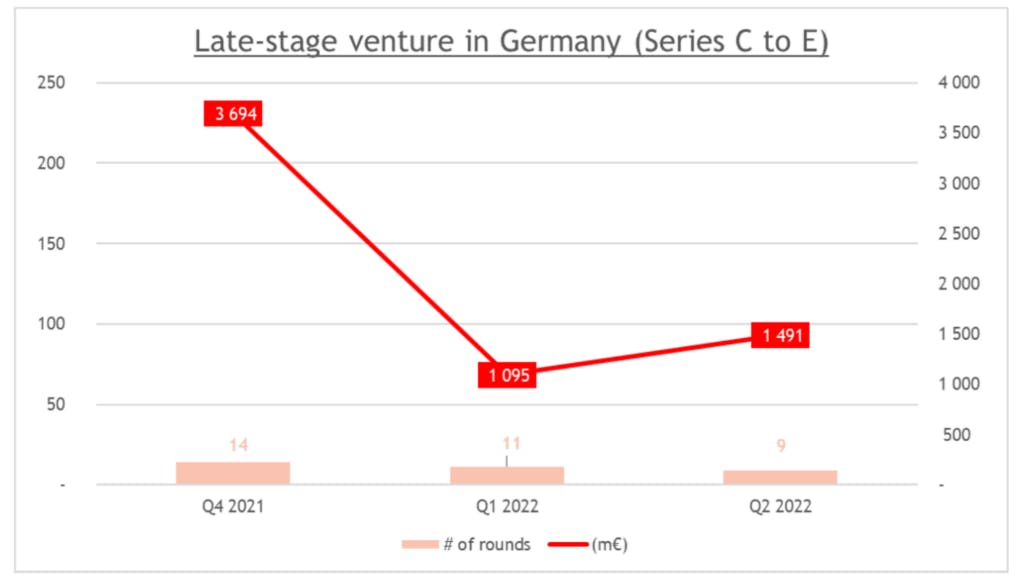

Ahead of France, Germany is among the first European countries to be hit and records a -56% volume drop at the end of Q1. Late-stage venture (series C to E) is the main driver: across the Rhine, the number of rounds is almost flat but volume is divided by more than 3. This can be explained by Germany being a more mature market and American investors historically more present than in France. As a consequence, with a total of €4.5Bn against €2.5Bn in Q1, France exceeds Germany in terms of total capital injected into its startups, and this for the first time since Q1 2020!

Source : Crunchbase

Euphoria however quickly fades: the wave reaches France with a quarter delay. April and May mark a clear decline, even more noticeable in value than in volume – with only two rounds over €100m (Alan and HR Path). Closing the first half of 2022, June performs unexpectedly for France. The €2Bn mark is passed again thanks to a hundred transactions. 5 companies raise more than €100m: Electra, Platform.sh, Flying Whales, and Ecovadis - which becomes the 28th French unicorn. Bottomline: over Europe in Q2, both the number of rounds and the volumes raised are cut by 30%. In Germany the quarter ends with a slow recovery, but investors remain extremely cautious.

Uneven impacts across stages and sectors – early-stage and climate on the rise

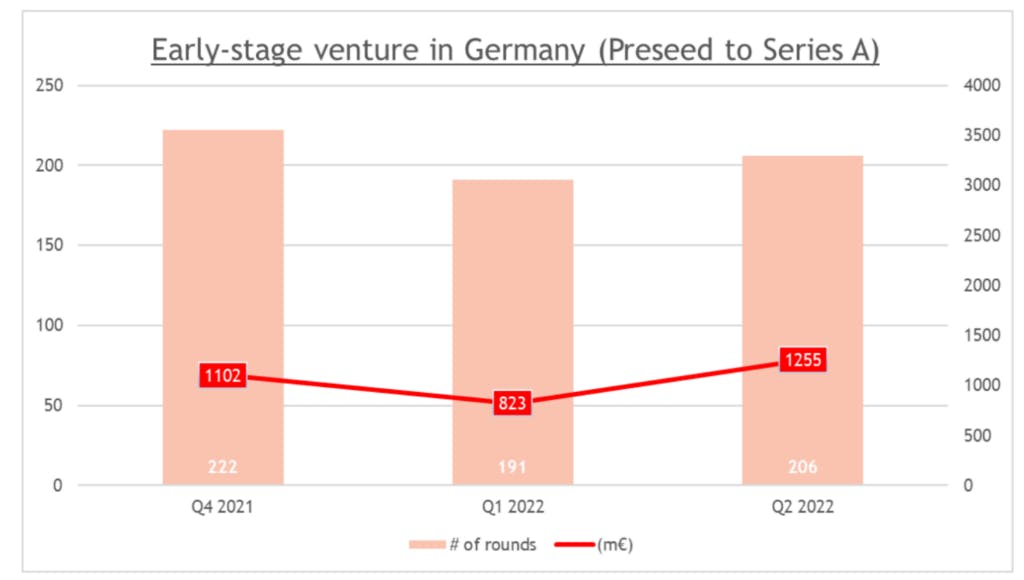

Late-stage rounds have undeniably slowed down, as illustrated by the reluctance of US fund Tiger, which has halved its investments since the end of Q1 2022. Valuations are down too. The most emblematic example in Europe is surely that of BNPL unicorn Klarna, which shed 12% of its staff and saw its valuation fall by a third at the end of May. As refinancings become more difficult, French and German investors alike are massively alerting their portfolios to the troubled months ahead. Non-essential expenses must be drastically reduced to extend the runway, and alternative sources of financing to equity must be considered: the use of debt and convertible bonds should be massively increased. Like the takeover of Cajoo by Flink, a wave of consolidation is to be expected. Early-stage however seems to resist in Europe over the first half of 2022. Compared to Q4 2021, the German market stumbled in Q1 (-25%) then recovered in Q2 and even recorded a slight increase (+13%). Late-stage investors partly deployed their capital in less risky early rounds instead.

Source : Crunchbase

If investors overall are much more cautious, not all sectors are equally affected. In the context of the global recession, customer-facing solutions could have a particularly difficult time. Conversely, fintech, cybersecurity or deep-tech startups may end up being relatively unscathed. Climate tech is a big trend of the last few weeks on both sides of the border and across all funding stages. 16 climate tech companies, from seed to Series C, received €1Bn fundings in France. In Germany alike, several seed rounds were announced, such as Caeli Wind, Charge Construct or Reverion. 2022 could be a remarkable year for climate tech! -- Stay tuned - tension in the public markets should continue to have an impact on the German-French venture capital market in the coming months. This situation raises the tricky issue of financial sovereignty, which both countries are tackling by recently reaffirming their willingness to support their tech ecosystems. Germany plans to mobilise up to €30bn in private and public capital while Emmanuel Macron set the objective of 100 French unicorns, including 25 "green" ones, by 2030...