Probably the first question that comes to mind when reading this title is why it is interesting from a European investor’s perspective to monitor Tier 1 US/UK funds behaviors. The answer lies in their ability to target and invest into future unicorns.

Since 2014, 62% of European unicorns and 70% of North American unicorns received funding by Tier 1 US/UK funds. (Pre 2014 it was 49% and 68% respectively). Now it’s hard to tell if the presence of Tier 1 US/UK funds attracts more investors, then leading to unicorn status, or if Tier 1 US/UK funds are great at selecting companies and sectors they invest in. Irrespective it can still be valuable for investors to understand their behaviors, as knowing which sectors/companies they like might help find the next major successes on European soil.

Methodology

To analyze current investment trends, we looked at funding rounds of 22 industry leading venture capital funds, the so-called Tier 1 funds (A comprehensive list can be found below). We limited our analysis to startups based in Northern America, Europe and Israel. We look at the timespan between 05/10/2020 and 05/10/2023.

The data of the funding rounds stem from Crunchbase. We categorized the startups based on 25 predefined sectors. For the categorization we gave Chat-GPT our 25 predefined categories and information about the startups such as their Website’s URL. Afterwards we sampled the accuracy of Chat GPT’s classification, and reclassified clusters manually where Chat GPT tended to misclassify. We performed the same exercise for the classification of our unicorns database. The data is from Crunchbase. We considered all companies as unicorns that Crunchbase tagged as such with Hub Tags.

Overall, we analyzed over 4500 funding rounds and over 900 unicorns.

Tier 1 US/UK funds

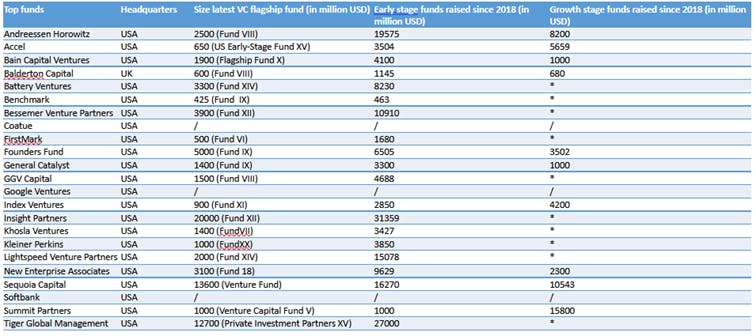

Here is a quick summary of the funds whose transactions we covered:

Figure 1 Tier 1 funds covered in this analysis and their recent fundraising activity (* represents that a VC performs growth stage investments and early stage investments out of the same fund).

Since European transactions only make about 15% of the combined transaction of Europe and North America, looking at Europe and North America combined would be highly skewed towards North America. Therefore, we will proceed by analyzing the funding trends individually.

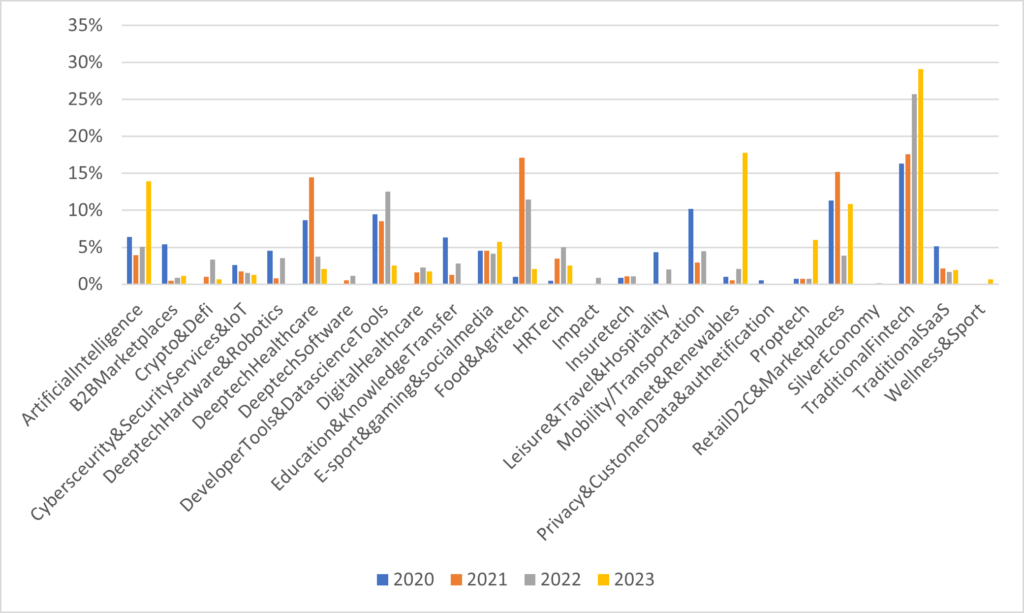

Recent Tier 1 US/UK fund investments in Europe

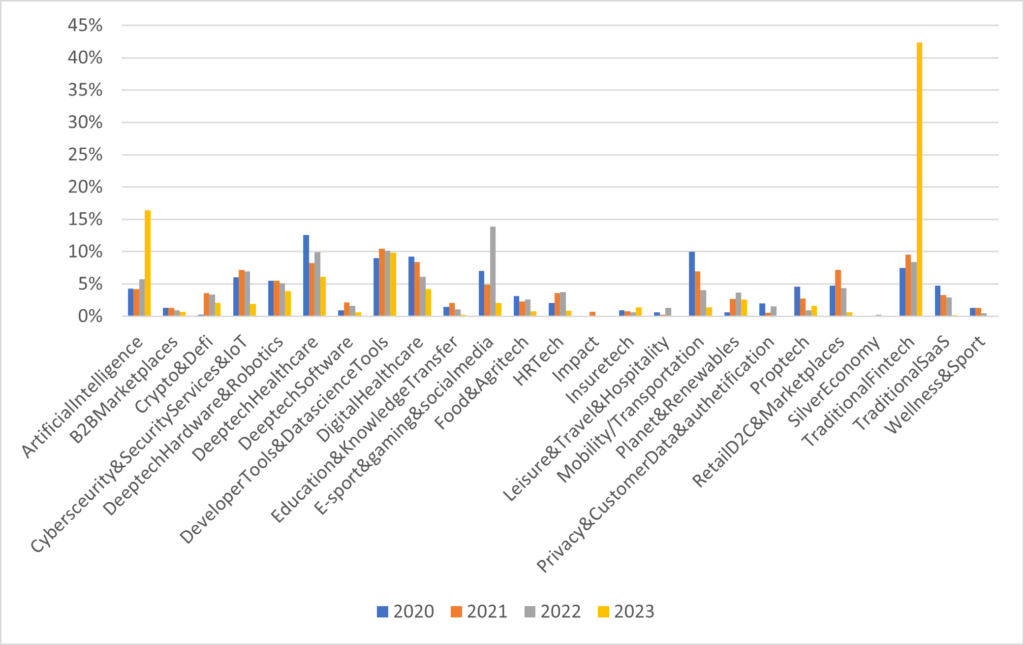

Figure 3 Share of investments by Tier 1 US/UK funds by sector, Europe, all funding stages.

To make the data comparable we don’t look at absolute amounts but rather at the share of investments in each sector in a given year. The intend of the graph is more to give information on how important a sector is to Tier 1 US/UK funds, rather than how well funded a sector is. This is a recurring theme throughout the analysis, the goal is to understand what areas Tier 1 US/UK funds deem the most relevant at the moment.

When looking at funding in Europe, among leading US/UK funds, fintech is the most popular and rising in popularity. Also on the rising, unsurprisingly, AI. Surprisingly, even with the respective decline of the hype of the metaverse, the share of investment in E-Sports, gaming and social media stays remarkably similar over the years. Deeptech healthcare becomes less popular, potentially in line with the decline of Covid-19. As a note the spike of planet and renewables is a result of the Series D round of Enpal and is thus not a fair indicator.

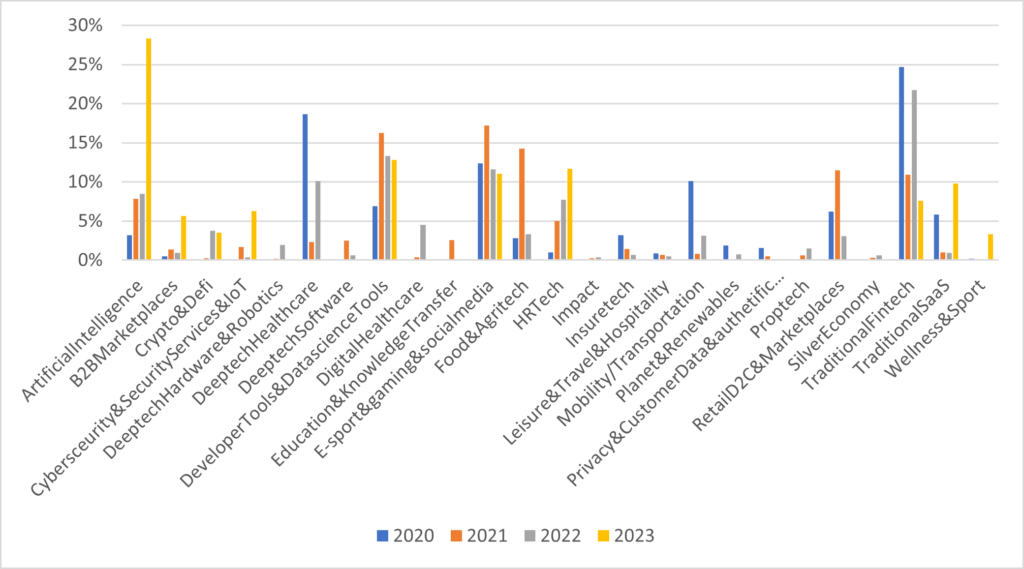

To better understand new funding trends among leading US/UK funds, it might be more interesting to look at the shares of funding in early-stage investments. In our case we considered early-stage investments as everything from Pre-Seed to Series B.

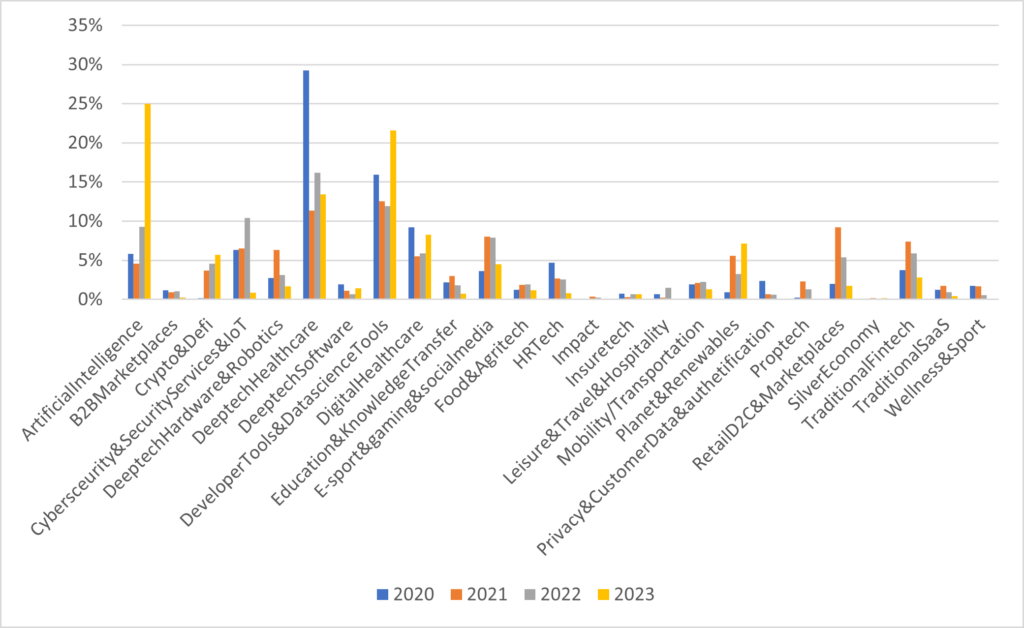

Tier 1 US/UK early stage investments by sector in Europe

Figure 4 Share of investments by Tier 1 US/UK funds by sector Europe early stage.

The picture changes a lot when we only look at early-stage investments, fintech is no longer a growing category but looks more like a category losing in popularity at Tier 1 US/UK funds. Similarly, there seems to be a downward trend in e-sports, gaming and social media. On the other hand the rise of AI becomes more visible. Furthermore, HR tech is becoming more favored by Tier 1 US/UK funds. Developer and data science tools are another very popular category for investments but show a declining share since 2021.

Recent Tier 1 US/UK fund investments in North America

Figure 5 Share of investments by Tier 1 US/UK funds by sector North America all stages.

When looking at the share of investments among all funding stages done by Tier 1 US/UK funds, we find that, similarly to Europe, AI is on the rise and deeptech healthcare is in decline. Furthermore, we find a significant decrease in the popularity of digital healthcare, as well as mobility and transportation. In contrast to Europe among all stages, Fintech is not on a clear growth trajectory, but flat for most years, the spike in 2023 is predominately due to Stripes latest funding round.

Similarly, to the methodology we used before, it might be more interesting to look at the shares of funding in early-stage investments in the US. In our case we considered early-stage investments as everything from Pre-Seed to Series B.

Tier 1 US/UK early stage investments by sector in North America

Figure 6 Share of investments by Tier 1 US/UK funds by sector North America early stage.

When only looking at Tier 1 US/UK funds early stage deals in North America, the rising popularity of AI becomes even clearer. Surprisingly, Crypto has slowly but steadily grown in popularity among Tier 1 US/UK funds. Cybersecurity has been growing from 2020 to 2022 but dipped in 2023. Overall developer and data science tools seem on a slight decline but spiked in 2023. In contrast to Europe, HR tech is becoming less popular in North America. Fintech is in decline since 2021.

Share of funding by Tier 1 US/UK funds by sector in each geography

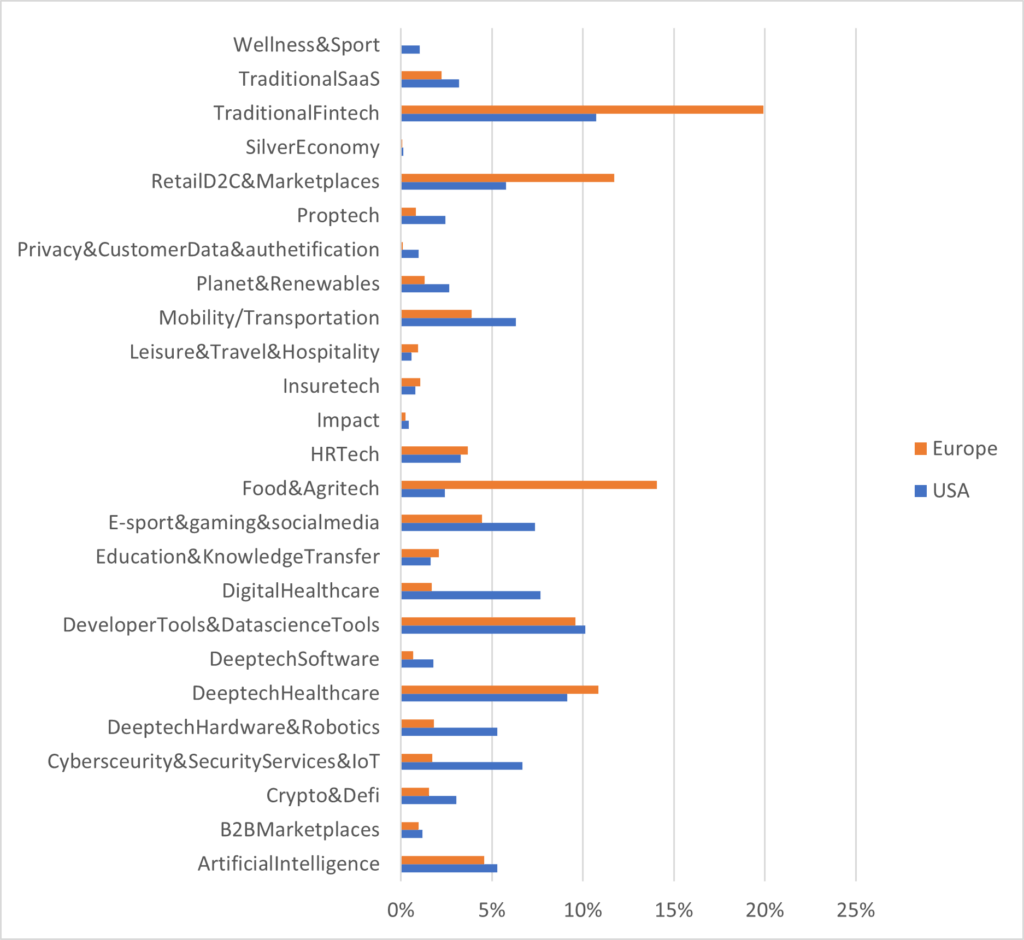

When comparing the relative funding received of each sector by leading US/UK funds in the given geography, we find that Tier 1 US/UK funds invest in Europe more aggressively in fintech, marketplaces and food and agritech (the latter is fueled by the European hype in grocery delivery startups). Whereas in North America AI, cybersecurity, mobility and transportation, e-sports and social media and digital Healthcare receive relatively higher attention by Tier 1 US/UK funds.

Figure 7 Share of funding by Tier 1 US/UK funds by sector in each geography, last 3 years all stages.

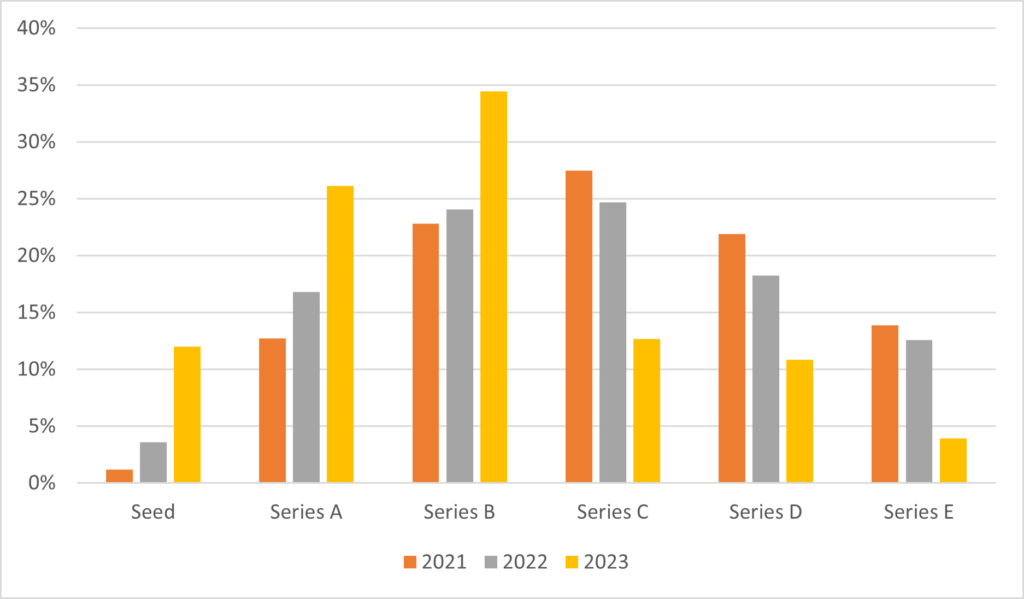

Furthermore, we found that Tier 1 US/UK funds have shifted towards earlier stage investments in recent years.

Figure 8 Share of money invested by investment stage Europe and North America.

Unicorns

Furthermore, we analyzed the concentration of Unicorns in each sector in both Northern America and Europe.

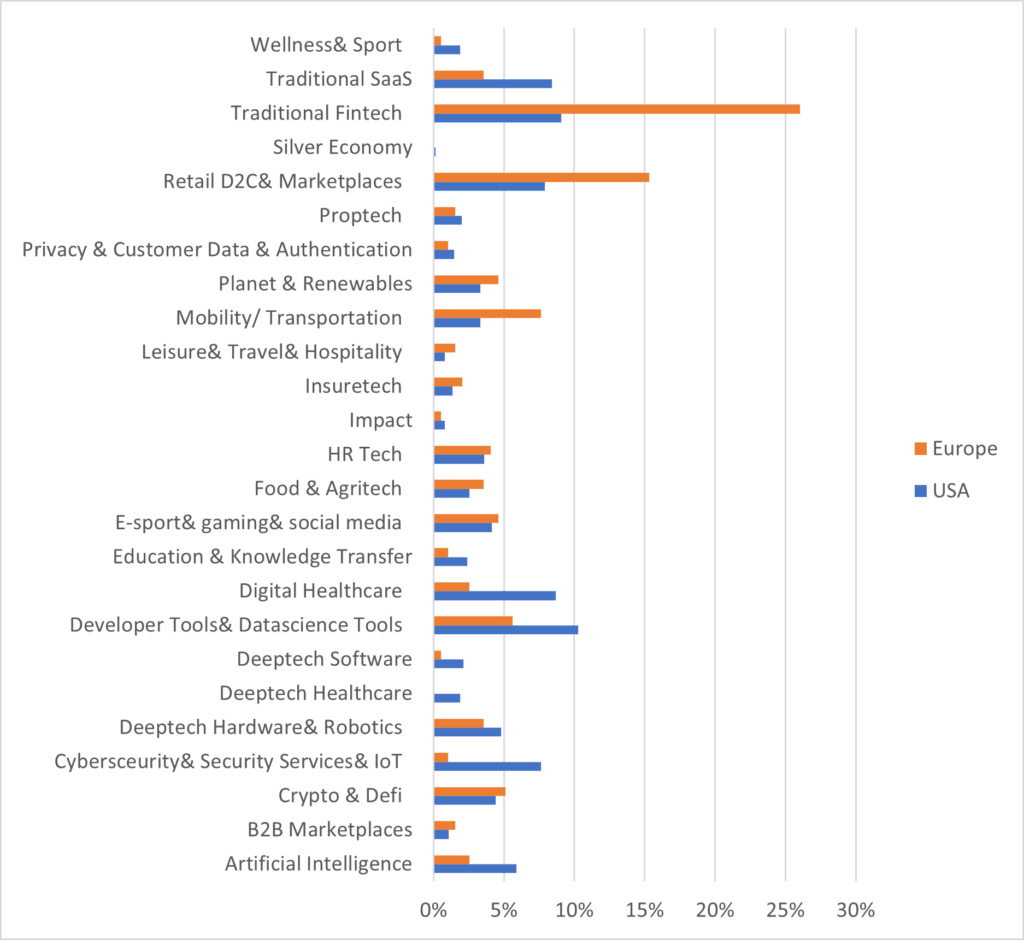

Figure 9 Share of Unicorns by sector, Europe and North America.

We find the sectors bringing up the most unicorns in North America were AI, developer tools and data science tools, cybersecurity, digital healthcare marketplaces, fintech and traditional SaaS. In Europe we find that two sectors stand out dramatically: Fintech and Marketplaces making over 40% of all European startups.

Further sectors with a high number of unicorns are mobility/ transportation, developer and data science tools as well a planet and renewables. We find that fintech and marketplaces as well as mobility are relatively more present in Europe than in Northern America. North America dominates in software related topics such as traditional SaaS, AI, cybersecurity, and developer tools. Looking at these two clusters we find that North America excels at topics that show high scalability with easy adaptation internationally. Whereas Europe’s relative strengths lie in sectors that are harder to enter as they offer a barrier of entry. In the case of fintech, it’s regulation and trust for mobility and planet and renewables it might be the need for additional production sites and regulation. So, to say Europe’s unicorns are relatively overrepresented in sectors where there is protection from American incumbents.

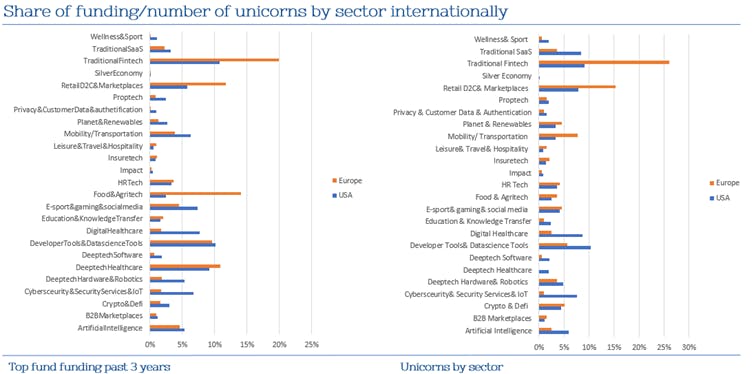

What’s very interesting to see is if you put Tier 1 US/UK funds’ investments in recent years against the distribution of unicorns there seems to be a similar distribution among sectors and geographies, apart from a handful of sectors. (One has to note that part of this effect might be due to the fact that investments done in the past 3 years led to the unicorn distribution we have today).

Figure 10 Share of investments by Tier 1 US/UK funds last 3 years vs share of unicorns by sector.

This led us to a potential implication, one might see the current distribution of unicorns as how good of a breeding ground for unicorns a certain sector was until now, and that if Tier 1 US/UK funds invest more heavily in a sectors than its past unicorn track record suggests, Tier 1 US/UK funds consider it to be a “hot” topic/ topic now able to produce more unicorns.

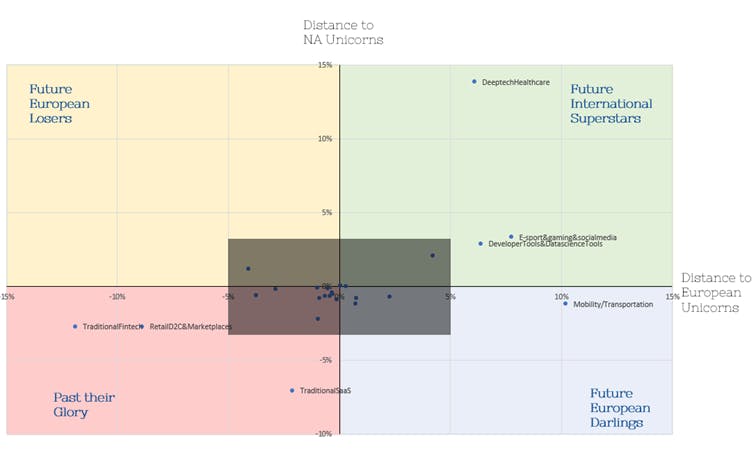

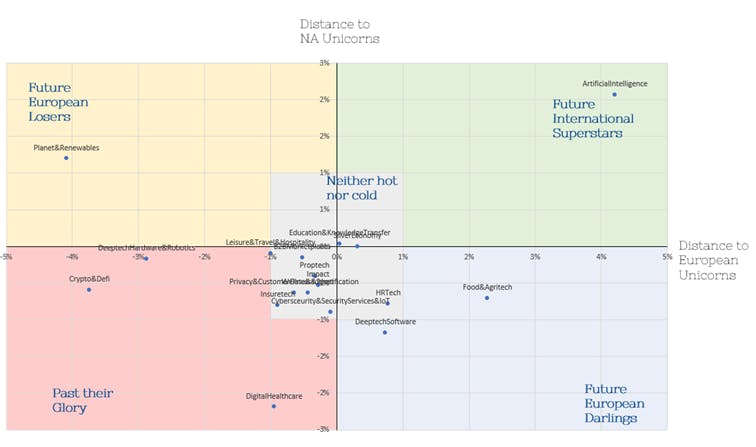

To map what sectors fall into this “hot” category, we computed the distance between the share of funding in the last 3 years by leading US/UK funds of each sector and its share of unicorns. Let me illustrate this on an example: AI raised 8% of the overall Tier 1 US/UK funds funding in the past 3 years in North America and presents 6% of unicorns in North America, therefore its y axis value is 2%. In Europe 7% of Tier 1 US/UK funds funding went into AI, whereas only 3% of unicorns are in the AI sectors, thus the x value of AI is 4%.

Figure 11 “Hot” Matrix.

So how is this to read? Future international superstar are sectors, which are considered hot by Tier 1 US/UK funds in both Europe and the North America. Future European darlings are funded more aggressively than in the past in Europe but underfunded in North America. Future European losers are sectors, that are funded more aggressively in North America than their past unicorn share would indicate but less aggressively than their European Unicorn share. Past their glory are sectors that don’t get as much attention by Tier 1 US/UK funds as their past unicorn share indicates.

The matrix gives a good indication of what sectors are considered as hot by Tier 1 US/UK funds and where. There are interesting potential implications that could be made for instance Future International Superstars could be sectors where a major technological shift might boost their investment interest. Whereas Future European Darlings might show sectors where a regional need makes this sector more interesting. However, these are just some possible implications, in some cases it can also be the case that certain sectors are addressed by a different kind of investor. For instance planet and renewables in Europe might be underinvested by Tier 1 US/UK funds, because impact funds go more into the topic, or this sector might be too regional for Tier 1 US/UK funds.

Acknowledgement

I would like to extend my sincere thanks to Arnaud Baraër, who had the impulse to investigate this topic and for his unparalleled support in this project, but also for his input when I wasn’t sure which way to go with in the analysis.