By Elsa Hayoun & Guillaume Meulle

In 2018, we highlighted the difficulties of the venture capital ecosystem in France in our article “A Venture Capital Funnel in Europe” following an analysis of first-time fundraisers in France between 2007 and 2009: an inefficient “Spread and Pray” strategy with weak graduation rate from first to second fundraising, early exits, and the lack of new unicorns that underscored the French ecosystem’s lag compared to the U.S.

Six years later, with 30 French unicorns and over €31 billion raised, the ecosystem seems to have undergone a transformation.

Today, we revisit this analysis to chek if the change in our ecosystem is really revealed in figures.

To address this question, we studied French startups that raised funds for the first time in 2019, using data from Crunchbase (so only “official” fundraisings). Five years later, their trajectories reveal what works—and what doesn’t—in the ecosystem.

Our Cohort

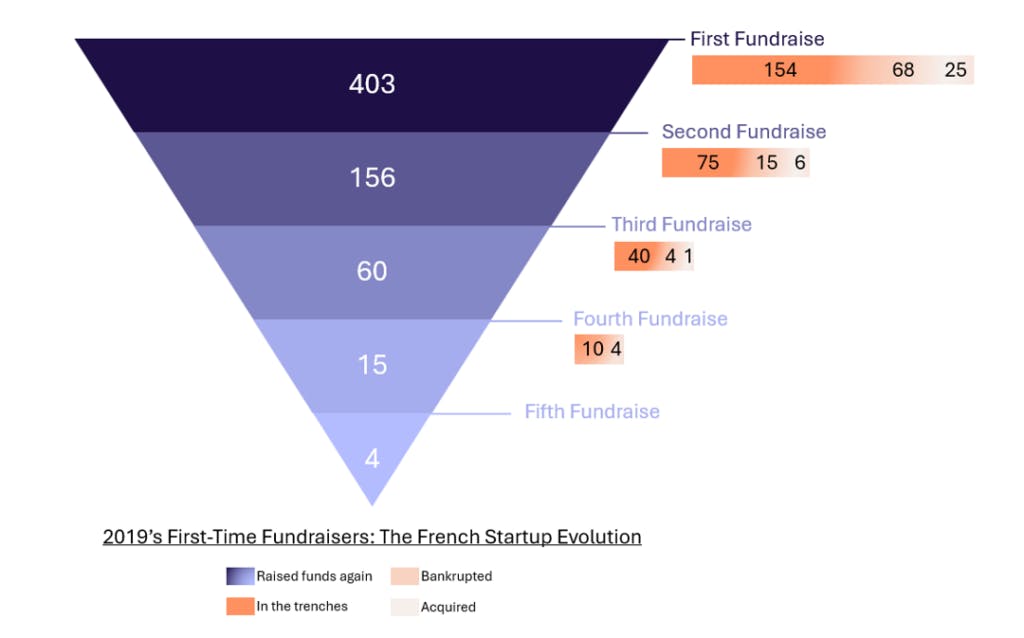

In 2019, 407 French startups (officially) raised funds for the first time.

Five years later, they have generated over 700 funding rounds, highlighting key dynamics of the ecosystem:

- Leading sectors: Fintech and healthcare dominate with twice as many funding rounds as IT or travel. Biotech and healthcare account for 16% of the sample.

- Funds raised: An average of €1.5M per round and €7.27M per startup. Sorare stands out with a record €680M raised in 2021.

- Startup survival: 70% remain active, 22% have stopped their activites, and 8% have been acquired.

- Impact of Tier 1 funds: Present in the first round for 22.6% of startups, their role grows in subsequent rounds, reaching 31% of funding.

The ecosystem demonstrates significant successes, but disparities remain strong across sectors and access to key investors.

What we found

a) Between 2007 and 2019, the French venture ecosystem has been transformed

- Yearly cohort of first time fundraising was multiplied by 5 in 10 years in volume

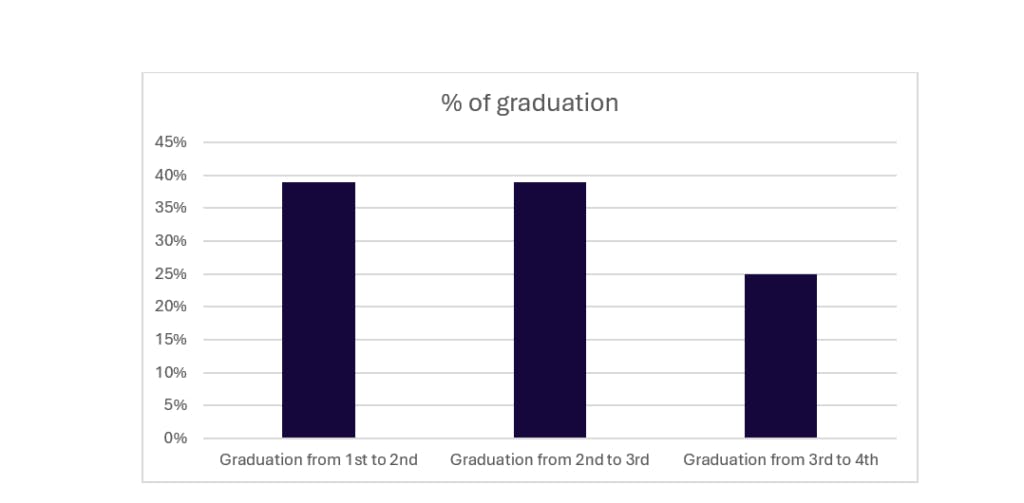

- While scaling in volume, graduation rate from 1st to 2nd fundraising increased from 30% to 39%

- Today, the ecosystem is more resilient: 70% of the startups in the cohort remain active, thanks to improved support and a strengthened entrepreneurial culture. However, acquisitions are less frequent (8% compared to 18% previously), likely due to easier access to funding and a slowdown in M&A activity since 2022.

b) Fundraising is a rollercoaster

The graph shows a stable or decrease in the frequency of fundraising rounds: 39% of startups graduate from first to second fundraising, 39% from second to third and 25% from third to fourth. At each stage, fewer and fewer startups manage to secure additional funding. It’s not because a startup reach a certain level that the job is done. It’s even the contrary!

This issue, already identified in 2018, highlights a persistent weakness in the French ecosystem: financing mature startups. While early rounds remain accessible, supporting their growth to achieve critical scale and compete internationally remains a major challenge.

c) No statistical factor determines a startup’s survival or fundraising ability

We analyzed several criteria to statistically evaluate their impact on the survival of startups and their ability to raise funds:

- Presence of a Tier 1 fund,

- Industry sector,

- Time between funding rounds,

- Total number of funding rounds,

- Total amount raised.

None of these factors demonstrated a significant correlation with the likelihood of survival or the ability to raise additional funds, regardless of the statistical models applied. This underscores a fundamental truth about venture capital: a startup’s success remains inherently unpredictable and cannot be fully explained through statistical analysis.

So for the moment venture capital can’t be reduced to a game of statistics.

What we now know

Thus, none of the factors studied directly influence the survival of French startups. The success and longevity of startups cannot be reduced to statistical models.

The increasing difficulty in raising funds, with less than 5% of the cohort securing a third round within five years, highlights a structural issue already identified in 2018 and still prevalent today: while early stages are often supported, financing growth phases remains a critical challenge for the French ecosystem. French companies might also take more time to grow due to a restrictive French & European market environment that limits early hypergrowth.