At XAnge, we’ve seen a noticeable influx of robotics startups at the early stage—founders rethinking autonomy, full-stack systems, and new applications across industry and infrastructure. At the same time, the broader European funding landscape is showing signs of a shift. After a muted couple of years, the first semester of 2025 brought rare early stage mega rounds back into view with Genesis AI raising $105M from a combination of US & European investors.

An exception or a new era? Let’s unpack the market dynamics shaping this moment.

After a Funding Dip, the Return of Mega Rounds?

After a decade of steady growth, European robotics hit a funding high in 2022, with over $1.1B poured into the sector; more than 3x the 2020 level. This “peak” was driven by a handful of blockbuster rounds, including Wayve’s $200M Series B and Daedalean’s $58M, both in the Autonomous Vehicle (AV) space.

But behind the headline numbers, cracks were already forming. Remove the mega-rounds, and 2022 actually saw the first drop in the number of funding rounds happening in robotics, foreshadowing the steady decline in dollars raised by robotics startups that followed. By 2024, robotics funding had hit a three-year low of $800M, and early-stage momentum had slowed considerably.

Now, in mid-2025, the tide may be turning. The first half of the year brought 65 deals—on par with the rate of investment in 2024—but this year’s funding raised to date already accounts for 75% of last year’s total funding amount. Capital is concentrating in fewer hands, with standout rounds like Neura Robotics’ €120M Series B early 2025 and Genesis AI’s $105M raising hopes of a new funding cycle. The rebound is uneven, and pre-seed and seed rounds remain small and sparse, with fewer sub-$4M deals than in S1 2023 or 2024, pointing to a widening funding gap for lesser known teams / early stage bets.

Lessons from the AV Funding Frenzy

Taking a closer look, much of the excitement seen during the 2022 robotics boom was actually concentrated in the autonomous vehicle (AV) space. Mega-rounds like Wayve’s $200M Series B inflated the numbers, but reflected a very specific type of robotics: capital-heavy, slow-to-deploy, and largely confined to self-driving, drones, and mobility infrastructure.

That first wave has since lost momentum. Progress toward full autonomy in open environments proved slower and more expensive than anticipated, and commercial traction has remained elusive.

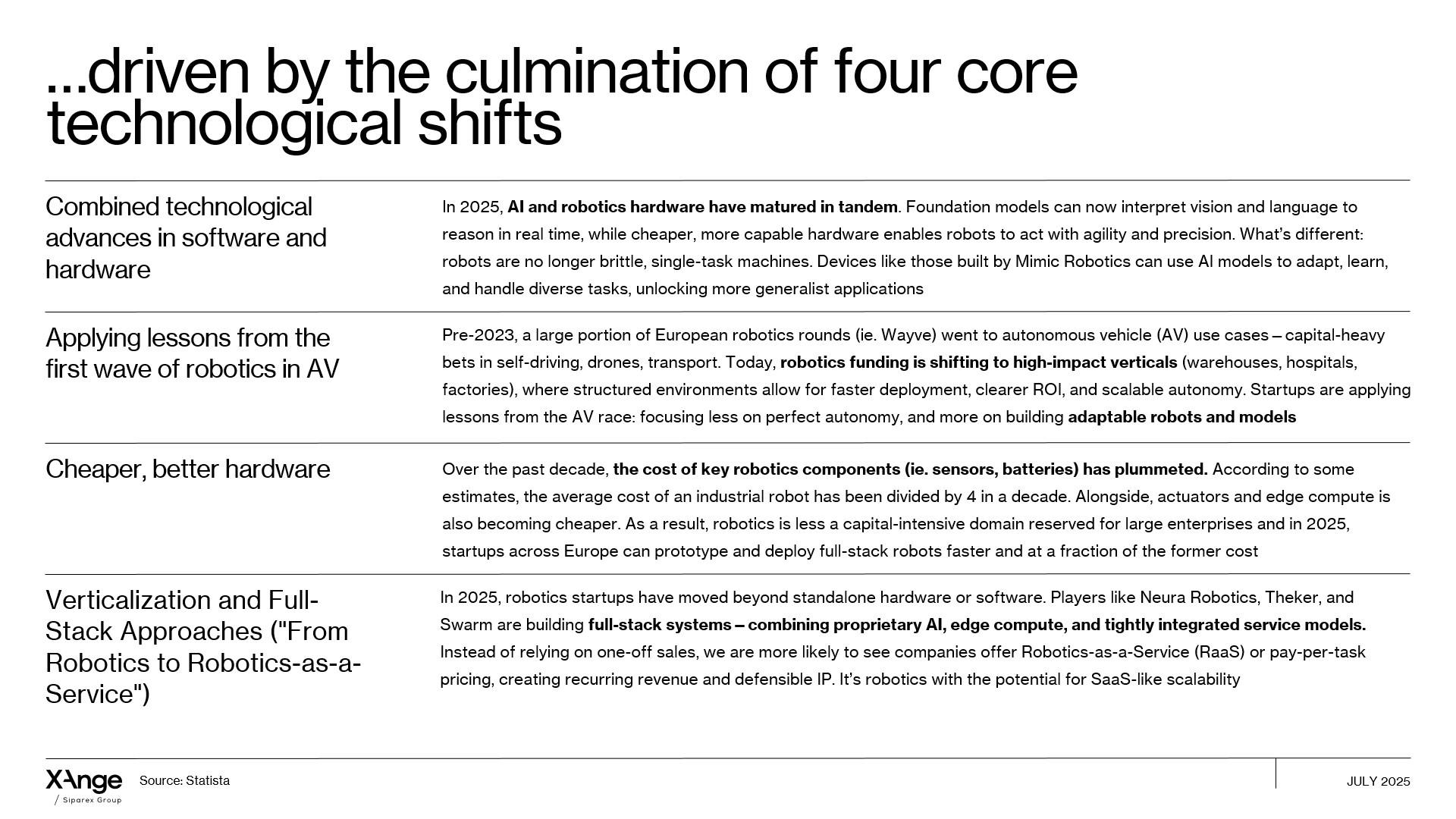

In 2025, the focus has shifted. Funding is flowing toward high-impact verticals like warehouses, hospitals, and factories—semi-structured environments where robotics can be deployed faster, deliver measurable ROI, and scale predictably. Startups are applying the hard lessons from the AV era: forget perfect autonomy, and build adaptable robots that work reliably in real-world conditions today.

What We’re Seeing Today: Mixed Expertise, Full-Stack Models, and the Software-Hardware Convergence

One of the most noticeable shifts in 2025 is what robotics startups look like under the hood. Pure hardware players / narrow software wrappers aren’t faring well. Today’s most promising teams combine deep domain know-how, AI & data and robotics engineering talent and building systems that are operationally scalable.

This evolution is enabled by the convergence of breakthroughs in both hardware and software. Foundation models now interpret vision and language in real time, while off-the-shelf sensors and compute modules make physical robots more agile, precise, and affordable. The future of robots doesn’t look like single-task machines. Companies like Mimic Robotics are developing generalist devices that can learn, adapt, and handle diverse tasks with minimal retraining.

We’re seeing a clear move toward full-stack, vertically integrated approaches. Startups like Neura Robotics, Theker, and Swarm combine proprietary AI, edge ops, and tightly integrated service models. Instead of selling hardware once, they’re offering Robotics-as-a-Service (RaaS) or pay-per-task models that drive recurring revenue and defensible moats—much like SaaS, but in the physical world.

Robotics startups are not just technical anymore, they’re strategic, deeply embedded, and built for compounding value. And it all starts with the right teams: cross-disciplinary, execution-focused, and fluent in both software abstraction and physical-world constraints.

The Landscape & Who We Are Watching

The European robotics landscape in 2025 is growing with a few standout players signaling where it’s headed. At the later stage, our portfolio company Wandercraft recently announed their $75M Series D to move from its first vertical in medical successes to build Calvin 40, their first industrial strength humanoids.

At the early stage, we at XAnge are paying close attention to startups building real-world applications with full-stack autonomy, deep tech roots, and the ability to scale.

Special thanks to Mohamed El Gamil for his contribution to this market map.